The Pharmacy Pulse Q1 2026 report provides an important snapshot of the current business environment for community pharmacies across Ireland, highlighting trends in prescription growth, over-the-counter (OTC) sales, operating costs, employment, business sentiment and merger and acquisition activity.

While many indicators point to continued growth and strong consumer demand for pharmacy services, the report also underlines the growing financial and operational challenges facing pharmacy owners.

Strong demand continues across the sector

One of the clearest messages emerging from the report is that demand for pharmacy services remains strong.

According to Central Statistics Office (CSO) data, the value of pharmaceutical sales increased by 3.9 per cent in March 2026 compared with the same period last year. IQVIA data also shows prescription (RX) classes increasing by 9.5 per cent in value and 5 per cent in volume, year-on-year.

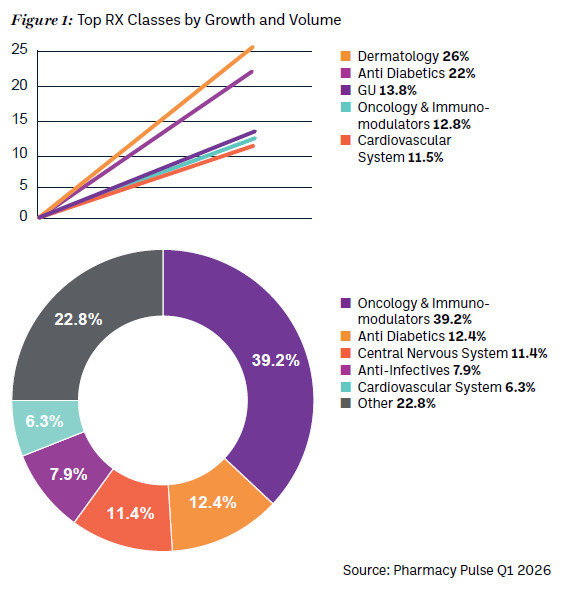

Several prescription categories recorded particularly strong growth. Dermatology products saw growth of 26 per cent, anti-diabetic medicines increased by 22 per cent, while genitourinary products rose by 13.8 per cent. Oncology and immunomodulator medicines also continued to represent the largest share of prescription value at 39.2 per cent.

These figures reflect wider demographic and healthcare trends, including an ageing population, increasing chronic disease management and continued demand for specialist medicines.

The OTC market presented a more mixed picture. While OTC sales values increased modestly by 1.5 per cent, volumes fell by 1 per cent, suggesting that inflation and pricing may be contributing more to value growth than increased consumer purchasing.

Pain relief products remained the largest OTC category by value, accounting for 26.4 per cent of sales, followed by cough, cold and respiratory products at 18.3 per cent. Digestive remedies recorded the strongest growth at 9.4 per cent, reflecting ongoing consumer focus on preventative health and self-care.

Image 1: Top RX Classes by Growth and Volume

Source: Pharmacy Pulse Q1 2026

Source: Pharmacy Pulse Q1 2026

Rising costs remain a major concern

Despite positive sales trends, rising operational costs remain one of the biggest concerns for pharmacy owners and managers.

The IPU quarterly survey found that 94 per cent of respondents experienced increased operational costs over the previous 12 months. Energy costs, wages and insurance were identified as the most significant areas of inflationary pressure.

More than a third of respondents reported energy cost increases of over 10 per cent, while wage growth also continued to place pressure on pharmacy businesses. Fitzgerald Power’s analysis showed wages rising by 5.36 per cent year-on-year, with insurance costs increasing by 5.63 per cent.

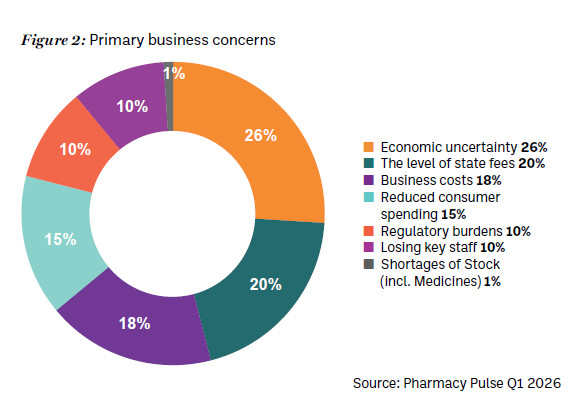

When pharmacy owners were asked about their primary business concerns, economic uncertainty ranked highest at 26 per cent, followed by the level of State fees at 20 per cent and general business costs at 18 per cent.

Image 2: Primary business concerns

Source: Pharmacy Pulse Q1 2026

Source: Pharmacy Pulse Q1 2026

The findings reinforce concerns across the sector regarding the sustainability of community pharmacy operations, particularly for smaller and independently owned pharmacies operating on tighter margins.

The report also highlights broader international risks which could further impact costs in the months ahead. A developing global energy crisis linked to geopolitical tensions in the Middle East has the potential to affect oil supplies and increase inflationary pressures internationally.

Business sentiment reflects cautious optimism

While many pharmacies continue to report improved turnover and increased footfall, confidence about the wider business environment remains cautious.

According to the survey, 43 per cent of respondents reported increased pharmacy footfall over the previous 12 months (a 22 per cent reduction), while 38 per cent said employment levels had increased with 13 per cent reporting a reduction. Sales and turnover performance also remained positive across most areas of pharmacy activity, particularly State dispensing and private dispensing services.

However, when asked about overall business prospects, 37 per cent of respondents said they felt less optimistic than 12 months ago, compared with 25 per cent who felt more optimistic. In addition, 44 per cent believed the current business environment was getting worse with only 23 per cent seeing an improvement.

This contrast between growing activity and declining confidence reflects the pressure many pharmacy owners are experiencing, as costs rise faster than income growth.

Mergers and acquisitions market remains active

The report also highlights continued strong activity in the pharmacy mergers and acquisitions market.

Fitzgerald Power estimates that eight pharmacy transactions were completed during the first quarter of 2026, matching the level of activity recorded during the same period in 2025.

Independent pharmacies accounted for the majority of transactions, underlining the continued attractiveness of owner-operated businesses to buyers. The report also identified a growing number of smaller pharmacies changing hands, suggesting increasing confidence and liquidity within the market overall.

Over the broader three-year period from 2023 to 2025, Fitzgerald Power estimated there were 98 pharmacy sector transactions nationwide, with the firm advising on 43 of those deals.

Regional trends also emerged from the data. Munster experienced a significant increase in transaction activity over the period, while Connacht and Ulster saw proportionally lower levels of deal activity.

Interestingly, PSI data showed no net increase or decrease in the number of community pharmacies nationally during the first three months of 2026, leaving the total number of pharmacies in Ireland at 1,916.

Looking ahead

The inaugural Pharmacy Pulse report provides a valuable benchmark for understanding the current state of Ireland’s community pharmacy sector.

The findings clearly demonstrate that pharmacies continue to play a vital role in healthcare delivery, with strong prescription growth, stable employment and sustained consumer demand underpinning the sector.

At the same time, the report highlights the growing pressure created by rising operational costs, uncertainty around funding and broader economic instability. For many pharmacy owners, balancing these challenges while continuing to invest in staff, services and patient care will remain a key priority over the coming years.

Importantly, the report also signals a sector that continues to evolve and adapt. Strong merger and acquisition activity, growing demand for healthcare services and ongoing engagement between sector stakeholders all point to a pharmacy sector that remains dynamic and resilient despite an increasingly complex operating environment.

As

Pharmacy Pulse develops into a quarterly publication, it is likely to become an important tool for benchmarking performance, identifying emerging trends and informing future policy discussions across the community pharmacy sector.

The

Pharmacy Pulse Q1 2026 Is available at

ipu.ie >

Publications >

Submissions & Reports.