A year ago, the key question of concern was how high interest rates would have to go to get inflation back under control, and the economic consequences that would result from the measures needed to get inflation back to a target range of around 2 per cent. Central bankers almost everywhere continued to tighten monetary policy into the summer months. Not surprisingly, as the year progressed global growth slowed down, with China, the UK and the Euro Zone showing distinct weakness. Consequently, the rate tightening ended in late summer and rates have remained on hold since then.

Early in 2023, it was widely expected that the US economy would go into recession in 2023, but in the event that economy surprised impressively on the upside. US growth was helped by the massive fiscal stimulus injected into that economy in recent years. At the same time, headline inflation rates declined at a faster pace than expected everywhere, due to a combination of higher interest rates, lower energy costs, and slower economic growth.

As we approach the end of the first quarter of 2024, the issues have changed. While China, the UK and Euro Zone are bouncing along the bottom, the US economy is still doing well. In general, there is a modest level of optimism for the global economy this year, but of course it is all relative. Inflation in the US has eased to 3.1 per cent; 4 per cent in the UK; and 2.6 per cent in the Euro Zone. It is steadily moving in the right direction, and consequently the speculation now concerns when central banks will start to cut rates and by how much. While it is always difficult to predict precisely what central bankers might do, it appears likely that the ECB will start to cut rates in the second half of the year, and we could see up to 2 per cent coming off rates over the next 18 months.

2024 can certainly be described as the year of the vote. 76 states around the world are due to have elections this year, including Russia and North Korea. Political events do tend to have significant economic consequences, so much of the focus on economics will be dominated by politics over the coming year.

There are elections to the European Parliament in June. The most interesting thing to watch in these elections will be the performance of the far-right, who are intent on destabilising the EU model. In Ireland, the European elections and the local elections in the same month will be watched closely for the economic manifestos of the various parties ahead of a general election that must be held by March 2025, particularly Sinn Féin. A general election is possible but not certain in the UK, but whenever it happens, a Labour government looks inevitable.

However, the most significant election promises to be the US presidential election in November. Donald Trump will win the Republican nomination, and if he manages to make it to the starting line due to legal considerations, there is a greater than 50/50 chance that he could become the next president based on current opinion polls. Such an outcome would have significant implications for the global economic order as barriers to trade in the shape of high tariffs and even more intense economic nationalism would likely become the order of the day. Trump would not be good for the global economy and global geo-political relationships.

In overall terms, 2023 was a reasonably good year for the Irish economy, but as always, Irish growth statistics require careful interpretation. Gross domestic product (GDP) declined by 3.2 per cent, signifying a technical recession. This was due to a decline of 4.8 per cent in exports of goods and services, which in turn was primarily driven by a decline of 4.9 per cent in the exports of chemicals and related products. This export correction is due to a post-covid normalisation in the sector, with lower value products now being exported compared to during COVID.

In 2023, consumer spending on goods and services increased by 3.1 per cent; tax revenues of €88.1 billion were collected, which is a record level and is €5 billion or 6 per cent ahead of the previous year — this was driven primarily by strong growth in income tax, VAT, and corporation tax; employment reached a record high of 2.7 million at the end of December; and the unemployment rate stood at 4.5 per cent at year end. It has subsequently fallen to 4.2 per cent in February, which is virtually full employment. Tax revenues in the first two months of the year were running 5.5 per cent ahead of the equivalent period last year, with income tax still particularly strong.

In overall terms, Ireland is still performing quite strongly, but housing, health, law and order, and immigration are dominating political discourse, and this will intensify over the coming months as the various domestic elections move closer.

The operating environment for the SME sector, particularly retail and hospitality, is becoming more challenging, not least due to Government measures. The costs of doing business continue to intensify. These Government measures include:

“While it is always difficult to predict precisely what central bankers might do, it appears likely that the ECB will start to cut rates in the second half of the year, and we could see up to 2 per cent coming off rates over the next 18 months.”

These factors are already, and will increasingly, impact on smaller businesses in particular.

Consumer spending softened somewhat as 2023 progressed, which is not surprising against a background of cost-of-living pressures and rising interest rates.

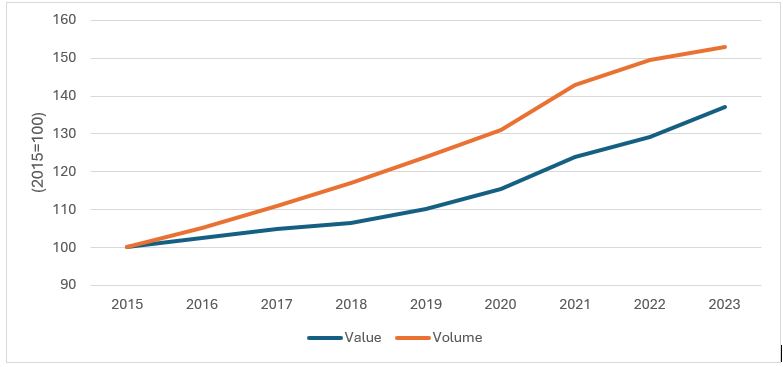

For 2023, the volume of total retail sales increased by 4.3 per cent and the value of sales increased by 8.8 per cent. Excluding motor trades, which distort overall retail spending (new car registrations were up a strong 15.6 per cent in 2023), the volume of sales increased by 1.1 per cent and the value of sales increased by 4.5 per cent.

In December, the volume of sales of pharmaceuticals, medical and cosmetic items increased by 0.4 per cent during the month and was 3.6 per cent higher than a year earlier. The value of sales increased by 0.7 per cent in December and was 7 per cent higher than a year earlier. For 2023, the volume of sales of pharmaceuticals, medical and cosmetic items increased by 2.2 per cent and the value of sales increased by 6.2 per cent.

Figure 1: Retail Sales of Pharmaceuticals, Medical and Cosmetic Items

Source: CSO

Source: CSO

Inflation and the escalating cost of living remained one of the more pressing challenges in the Irish economy during 2023. For 2023, average consumer prices increased by 6.3 per cent. In January, the average rate of inflation stood at 4.1 per cent, which is down from a peak rate of 9.2 per cent in October 2022. The likelihood is that the annual rate of inflation should gradually ease towards 2 per cent during 2024.

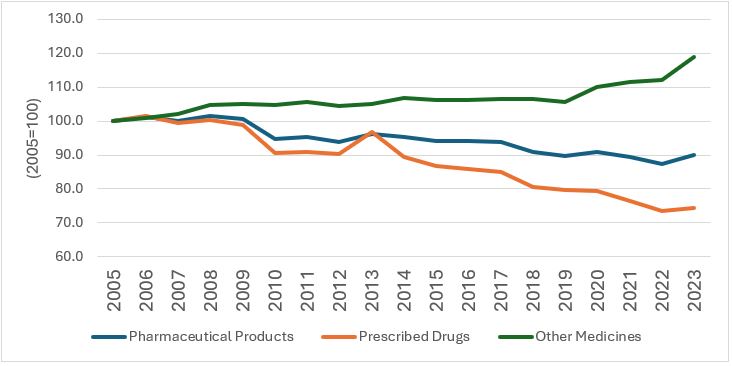

After a prolonged period of price deflation in the pharmacy sector, average consumer prices have increased over the past year. In the year to December, the average price of pharmaceutical products increased by 3.7 per cent, with the average price of prescribed drugs increasing by 2.2 per cent and the average price of other medicines increasing by 6.4 per cent.

For 2023, the average price of pharmaceutical products increased by 3 per cent, with the average price of prescribed drugs increasing by 1.2 per cent and the average price of other medicines increasing by 6.3 per cent.

Figure 2: Average Consumer Price Pharmaceutical Products

Source: CSO

Jim Power hosts a pop

Source: CSO

Jim Power hosts a pop