The IMF (International Monetary Fund) published its latest World Economic Outlook in mid-April. In its four published official forecasts during 2022, it revised down its global growth forecast for 2023 on every occasion. However, in January this year it upgraded its forecast in a modest way, from 2.7 per cent to 2.9 per cent. Despite the modest upward adjustment, it was symbolically significant, coming as it did after four consecutive downgrades. The upward revision was due to the lifting of COVID restrictions in China and the fall in global energy prices since last Autumn. This marked a significant improvement in global economic confidence, and this became the mood music in the first two months of the year.

Unfortunately, that mood music has changed again in recent weeks. In the April forecast, the IMF revised its global growth projection for 2023 from 2.9 per cent to 2.8 per cent. This is a very modest downgrade, but the accompanying narrative was extremely negative. It suggested that the prospects for a soft landing for the global economy are fading. A soft landing describes inflation coming down and growth remaining steady. It believes that the risks to the global economy are now on the downside. The negative forces include stubbornly high inflation; financial sector turmoil (the banking difficulties seen in recent weeks); government debt levels are high, which in theory should limit the ability of governments to provide fiscal support (that is the view of the fiscally conservative IMF); the Ukraine war is ongoing; global geo-political tensions are high; and interest rates have been tightened significantly over the past year, and they are likely to rise further.

In summary, the IMF believes that the risks of a hard landing are now elevated. However, despite the negative prognosis, it is forecasting unemployment to remain low and labour markets to remain tight, and inflation to ease in 2024.

Central to the IMF’s more negative prognosis is the global banking background. Markets and general sentiment took a hit in March when banking difficulties came to the fore again. Three medium-size banks in the United States have been shut down and the Swiss bank, Credit Suisse (CS) has had to be acquired by its larger competitor, UBS. It is of course possible to argue, as has been done, that these banks all have unique issues that are not reflective of overall global banking. However, the reality is that after a year of aggressive monetary policy tightening, some significant balance sheet problems have been created for many banks.

It is possible that further banks will get into difficulty over the coming months. However, it is important to bear in mind that central banks and policy makers in general will continue to respond aggressively to seek to contain these banking problems, as happened in the United States and Switzerland. Nevertheless, there is likely to be a sense of nervousness over the coming months as the reality is that a move away from the intoxicating effects of artificially low interest rates and a decade of quantitative easing was always going to give rise to problems and challenges. It is not 2008, but it still feels uncomfortable. The balance sheets of the Irish banks look solid, but contagion is always a fear in financial markets.

On the interest rate front, the ECB increased rates by 0.5 per cent in March, taking its base rate to 3.5 per cent. This stood at zero as recently as last July. In recent weeks ECB officials have suggested that they will now be monitoring economic and inflation data over the coming weeks before making any decision about a further interest rate increase at the May meeting. However, the bias is still towards further tightening. A 4 per cent base rate seems realistic over the coming months.

The Irish economic performance continues to be solid so far in 2023. Tax revenues totalled €19.7 billion in the first quarter and were 14.6 per cent ahead of the first quarter of 2022. Income tax expanded by 8.1 per cent; VAT by 15.9 per cent; and corporation tax by 71.4 per cent. The Exchequer recorded a deficit of €2.1 billion in the quarter, but this due to the transfer of €4 billion into the National Reserve Fund (rainy day fund). There is now €6 billion in that fund.

The unemployment rate stood at 4.3 per cent of the labour force in March, with 117,200 people officially registered as unemployed, which represents a decline of 14,400 on March 2022. The labour market remains very tight.

Against a background of rising interest rates, there are clear indications that residential property price inflation is continuing to decelerate. In the year to January, national average residential property prices increased by 6.1 per cent, with prices in Dublin rising by 4.3 per cent and prices outside Dublin rising by 7.4 per cent. These growth rates are down from a peak growth rate of 15.1 per cent in national average prices in March 2022; a peak growth rate of 13.2 per cent in Dublin prices in February 2022; and a peak growth rate of 17.1 per cent in the rest of Ireland in March 2022.

Between November 2022 and January 2023, national average residential property prices declined by 0.4 per cent; and between September 2022 and January 2023, average residential property prices in Dublin declined by 1.7 per cent. Housing remains the most significant challenge facing the country.

Looking out over the remainder of the year, the risks to Irish economic growth are obvious. The external environment is very uncertain, as evidenced by the latest IMF forecast; interest rates are set to increase further; the cost-of-living pressures are still intense; the costs of doing business are elevated; the housing market is in deep crisis and poses a significant threat to the economic competitiveness of the economy; global geo-political developments are creating massive uncertainty and potential instability; and the global technology sector is cutting costs and shedding labour, and this is likely to have some impact on corporation tax revenues and employment here.

On the positive side, the economic momentum at the end of the first quarter is still strong; employment is at a record high and there is a full-employment level of unemployment; the FDI performance is holding up well; the Irish banking system is stable, with solid balance sheets, but their cost of funding will now increase due to global developments; the public finances are strong; and there is a record level of household deposits at €148.4 billion in January 2023. The Irish economy looks to be in a strong position facing the external challenges, but some easing of activity seems inevitable over the remainder of 2023.

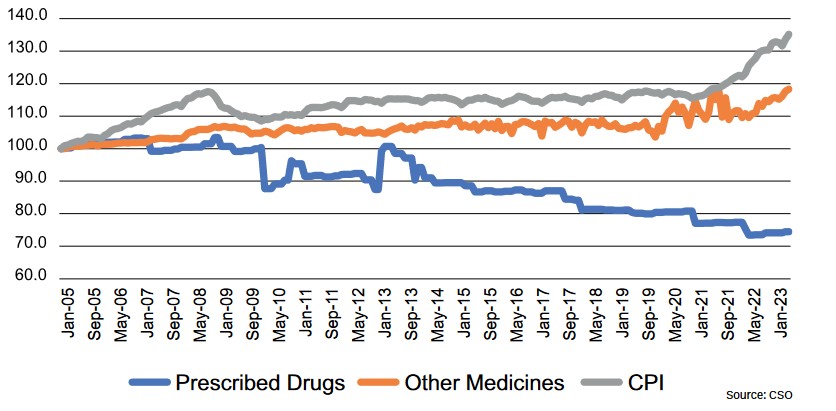

Inflation continues to be a dominant theme. In the year to March, average consumer prices increased by 7.7 per cent. This is down from a peak of 9.2 per cent in October 2022. The decline in the headline rate is due to lower oil and natural gas prices. In the year to March the average price of food increased by 13.3 per cent; private rents were up 10 per cent; airfares up 35.6 per cent; and accommodation was up by 19.1 per cent. In contrast, the average price of pharmacy products increased by 4 per cent, with prescribed drug prices up by 1.4 per cent and the price of other medicines up by 7.9 per cent.

Source: CSO

In the first two months of the year, the value of overall retail sales increased by 10.9 per cent and the volume of sales increased by 3.3 per cent. A solid consumer performance, with higher prices boosting the value metric. Within the pharmacy sector, the value of retail sales of Pharmaceuticals, Medical and Cosmetic Items increased by 7.4 per cent and the volume of sales increased by 4.2 per cent. Inflation in the sector is increasing but is still behind the average rate of price increase.