2025 was a remarkable year in terms of global politics and indeed economics. President Trump assumed office for the second time, and he hit the ground running. Much stands out from his first year in office, but from an economic perspective, everything revolved around the threat and actualisation of tariffs, albeit the rates eventually applied were not as severe as he initially threatened in most cases.

The policy towards tariffs created significant uncertainty, but despite this, the global economic performance turned out better than expected and the global economy proved quite resilient in the face of so much uncertainty. Global growth surprised on the upside but was still below trend. The main factors behind the more resilient global performance included a boom in AI-related investment; improved financial conditions, with bond and equity markets largely well behaved; lower official interest rates in the US, UK and Euro Area, and a number of other countries around the world; a front-loading of exports ahead of threatened tariffs; and significant fiscal stimulus in several countries, but particularly in China, Germany and the US.

International forecasting agencies were surprised by growth in 2025, but fear that the real impact of tariffs will be felt in 2026. This remains to be seen and is not a certainty. Lower interest rates in the US and UK, and ongoing fiscal expansion will continue to provide support to growth over the coming year. The tax cuts and rebates included in the ‘one big, beautiful bill’ in the US will be particularly important for the US economy.

The ECB left rates unchanged at its December meeting, and rates have now been on hold since the last cut in June. The ECB appears happy that it has rates at an appropriate level and is in no mind to alter rates in either direction for the near future. It will just monitor growth and inflation over the coming months before making any further interest rate decisions.

2026 has started off with a bang and the geo-political uncertainty and turmoil that characterised 2025 has carried over, with Venezuela, Iran and Greenland currently dominating the agenda. Where any of these issues go from here is anybody’s guess, but global geo-politics will dominate the agenda, just as they did in 2025.

The general expectation from forecasting agencies is that global growth will be slightly weaker than in 2025, reflecting the impact of tariffs. It appears that the key issues to watch over the coming year include: the sustainability of the AI investment boom and the implications for equity markets; bond market volatility driven by fiscal deficits in countries such as the US, Italy, France, and the UK and the appointment of the next Chair of the Federal Reserve in May; the relationship between China and Taiwan; the behaviour of Russia and its reaction to ongoing EU support for Ukraine; the necessity to increase defence spending everywhere; growing anti-immigrant sentiment around the world; the relationship between the US and Venezuela, and the possible implications for other Latin American countries and Greenland; the increasing sophistication of cyber terrorism; extreme weather events; and there are a number of important elections around the world. The US mid-term elections on 3 November will attract most attention. In other countries where important elections are being held, such as Sweden, Brazil, Colombia, Hungary, Japan, and local elections in the UK, the performance of more extreme political actors will be watched with interest.

2026 promises to be an interesting year and global geo-political developments will continue to give rise to deep concern.

The Irish economy delivered another solid performance in 2025, as evidenced by a strong labour market; robust growth in tax revenues; a strong export performance; and reasonable consumer spending.

Official growth data for the first nine months of the year show that GDP expanded by a strong 15.8 per cent. However, GDP is not a reliable indicator of economic activity in an Irish context as it is grossly exaggerated by factors such as IP investment, repatriated profits, and aircraft leasing. Modified domestic demand is a more realistic indicator, and it expanded by 4.1 per cent in the first nine months, with consumer spending on goods and services growing by 2.9 per cent.

The Irish labour market continued to perform strongly in 2025. In the year to the third quarter, employment increased by 30,600 to reach a record high of 2.825 million. From quarter to quarter the sectoral employment levels can be quite volatile. In the third quarter, the ICT sector saw employment decline by 8,000, and accommodation and food services decline by 8,700. Both trends will need to be watched carefully going forward.

Despite the continued strength of the labour market, the growth in employment moderated as the year progressed, and the unemployment rate edged upwards. In December, the unemployment rate stood at 5 per cent of the labour force, up from a rate of 4.5 per cent a year earlier. In December 2025, 148,700 people were officially unemployed, which is up 19,700 from a year earlier.

In December, the IDA reported its results for 2025. A record number of new investments were approved at 323, which is 14 per cent higher than in 2024. At the end of 2025, employment at IDA-supported companies reached 312,400, which is an increase of 1.5 per cent on 2024.

As we move into 2026, the momentum in the Irish economy is still solid, but there are several relevant considerations for the year ahead and beyond. These include the requirement to make real progress in addressing the housing crisis; the inordinate dependence on FDI and the threat posed by US policies; addressing water and energy issues; and the inflated costs of doing business.

The operating environment for the SME sector is challenging. In 2026, the cost environment is likely to deteriorate further due to the increase in the minimum wage; the PRSI increase; auto-enrolment; and further energy cost rises are likely. Budget 2026 did little to provide support to the sector, with the reduced 9 per cent VAT rate not applicable until 1 July. It is essential that more support is given to the SME sector and that its real contribution to regional economic activity is fully appreciated.

The economy looks set to deliver another solid year in 2026, although some modest weakening of the labour market is likely. Growth of around 2.5 per cent in the real economy looks achievable, which would represent a solid outturn.

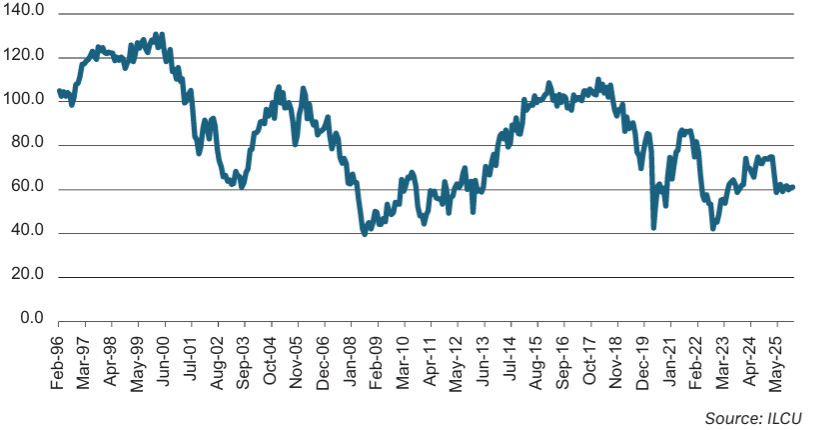

“2026 has started off with a bang and the geo-political uncertainty and turmoil that characterised 2025 has carried over, with Venezuela, Iran and Greenland currently dominating the agenda. Where any of these issues go from here is anybody’s guess.”Figure 1: Consumer confidence

For the Irish consumer, the key economic and financial trends that impacted on their lives in 2025 included a further decline in interest rates; a continuation of the savings habit as demonstrated by the €170 billion sitting on deposit in the banking system earning negative real returns; very modest tax reliefs for workers stemming from Budget 2025; a further deterioration in the cost-of living situation; and another very strong year for equity market investors.

Looking out to 2026, some of these trends will still be evident. The savings habit and risk averse behaviour should continue to characterise savers, and inflation will continue to eat away at real purchasing power. On the other hand, interest rates may fall modestly in 2026, but the ECB appears more likely to keep rates on hold. The real burden of tax for income tax- payers will increase following Budget 2026, which the ESRI estimates will reduce disposable incomes by 1.5 per cent in 2026. The cost of housing to buy or rent is likely to rise further, although the pace of increase should logically moderate. Around 800,000 employees are likely to be enrolled in the new pension scheme, which will increase costs for SMEs and undermine disposable incomes for those enrolled. Services such as health insurance, hairdressing, and eating out are likely to become even more expensive, despite the 9 per cent VAT rate in July.

2025 was, in general, a challenging year for the retail sector. Consumer confidence weakened during the year in the face of cost-of-living pressures, tariff-related concerns, and the failure to deliver any tax concessions for workers in Budget 2026. In the first 11 months of the year, the volume of retail sales was 2.3 per cent ahead of the same period in 2024, and the value of sales expanded by 2.9 per cent. When the motor trade is excluded, the volume of sales increased by 1.4 per cent and the value of sales expanded by 2.1 per cent. This describes a modest retail sales environment.

In the first 11 months, the volume of retail sales of pharmaceutical, medical, and cosmetic articles was 2.7 per cent up on a year earlier, and the value of sales was up by 3.7 per cent.

The annual rate of inflation bottomed out at 1.7 per cent in July 2025 and subsequently accelerated to reach 3.2 per cent in November. This is the highest annual rate since February 2024. In the first 11 months of the year, inflation averaged 2.2 per cent. Within the pharmacy sector, the price of pharmaceutical products increased by 0.9 per cent in the year to November, with the price of prescribed drugs increasing by 1.4 per cent, and other medicines by 0.1 per cent.

Jim Power is an independent economist and co-host of The Other Hand podcast.